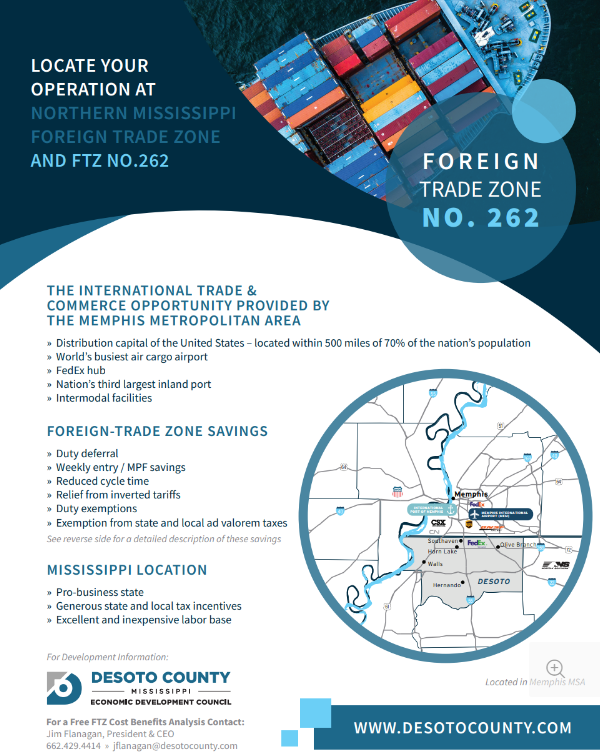

The International Trade & Commerce Opportunity Provided By the Memphis Metropolitan Area

- Distribution capital of the United States – located within 500 miles of 70% of the nation’s population

- World’s busiest air cargo airport

- FedEx hub

- Nation’s third largest inland port

- Intermodal facilities

Foreign-Trade Zone Savings

- Duty deferral

- Weekly entry / MPF savings

- Reduced cycle time

- Relief from inverted tariffs

- Duty exemptions

- Exemption from state and local ad valorem taxes

Mississippi Location

- Pro-business state

- Generous state and local tax incentives

- Excellent and inexpensive labor base

Foreign-Trade Zone Savings

Duty Deferral

No Customs duty is charged on merchandise while it is in a Foreign-Trade Zone, and there is no limit on the length of time merchandise may be kept in a Foreign-Trade Zone. Customs duty is paid only when the merchandise exits the zone and enters the commerce of the United States. By deferring the duty, capital is freed for more important needs.

Inverted Tariff Relief

Generally, if a foreign component is brought into a Foreign-Trade Zone or Subzone and manufactured into a product that carries a lower Customs duty rate, then the lower rate applies to the foreign component.

Weekly Entry / MPF Savings

The current Customs Merchandise Processing (User) Fee (MPF) of .3464% (.003464) ad valorem is only applicable to the value of foreign non-duty paid merchandise imported into the Customs territory of the United States. The North American Free Trade Agreement provides that the fee is zero for Canadian/Mexican NAFTA qualifying merchandise. The fee is payable with the filing of the entry summary (CBPF 7501) for a Customs consumption entry (entry type “06” and “08”). Merchandise that is scrapped, exported, or removed on a CBPF 216 or an in-bond transfer from the zone is not subject to the Merchandise Processing Fee. The MPF fee has a minimum of $26.79 and is capped at $519.76 per Customs consumption entry.

Reduced Cycle Time

Delays relating to U.S. Customs clearances are eliminated. Special direct delivery procedures expedite the receipt of merchandise in company facilities, reducing inventory cycle time.

Duty Exemption on Exports

If imported merchandise is exported after being placed in a Foreign-Trade Zone or shipped to another Foreign-Trade Zone and then exported, no Customs duty is ever paid.

Duty Elimination on Waste & Scrap

No Customs duty is charged on most waste and scrap from production in a Foreign-Trade Zone.

No Duty on Rejected or Defective Parts

Merchandise found to be defective or faulty, may be returned to the country of origin for repair or simply destroyed. Whichever choice is made, no customs duty is paid.

Exemption from Local Ad Valorem Taxes

Foreign merchandise stored in Foreign-Trade Zones, or merchandise held in a zone for export, is not subject to any state or local ad valorem tangible personal property taxes.

No Duty on Domestic Content or Value Added

The “value added” to a product in a FTZ (including manufacturing using domestic parts, costs of labor, overhead, and profit) is not included in its dutiable value when the final product leaves the zone. Final duties are assessed on foreign components only.

No Duty on Sales to the U.S. Military or NASA

No duty is charged on foreign merchandise sold from a Foreign-Trade Zone to the U.S. Military or NASA.

Jim Flanagan

President/CEO

DeSoto County Economic Development Council

4716 Pepper Chase Drive

Southaven, MS 38671

Office: 662-429-4414

jflanagan@desotocounty.com